This year, the Department of Education has been working out issues with the new version of the Free Application for Federal Student Aid (FAFSA), which was slated to be released in late December. While the form is now available, the Department pushed back the transfer of FAFSA data to colleges until early March of 2024. Understanding the changes in financial aid has been challenging, given the newness of the form. Still, the information below will help you understand the basics of financial aid and how to maximize your chances of receiving grants and low-interest loans.

Let’s Start with Some Terminology

General Key Terms

- Cost of Attendance (COA) or “Sticker Price”: The combined cost of attending a school—including tuition, books and supplies, food and housing, transportation, and other personal expenses—before financial aid is applied.

- Net Price: The actual cost of attending a school after scholarships & grants are subtracted from the sticker price/COA.

Types of Financial Aid

When financial aid is awarded to students, it’s either in the form of gift aid or loan aid.

- Gift Aid: Financial aid that does NOT need to be paid back (aka, free money!) Examples include: scholarships, grants (sums of money that institutions distribute largely based on a family’s financial information) and Federal Work-Study. FWS is a federal program that provides students with the opportunity to work part-time on campus to earn money that they can use to pay school-related expenses. This type of aid is NOT automatically applied to the student’s bill; to see if the school will allow you to apply FWS funds to your bill directly, contact your school’s financial aid office.

- Loan Aid: Financial aid that must be repaid, either while the student is in school or after they graduate. Examples include federal loans (provided by the federal government) and private loans (loans provided by various sources, including the institution itself, banks, or credit unions).

Financial Aid Applications

There are two major financial aid applications that all students and families should be aware of: the FAFSA and the CSS Profile. Let’s discuss some key terms associated with each application.

- Free Application for Federal Student Aid (FAFSA): A financial aid application administered by the US Department of Education that determines a family’s eligibility for federal grants and loans, as well as state and/or institutional aid. The FAFSA is required for all students seeking federal aid, but it is recommended that ALL students complete this application as early as possible!

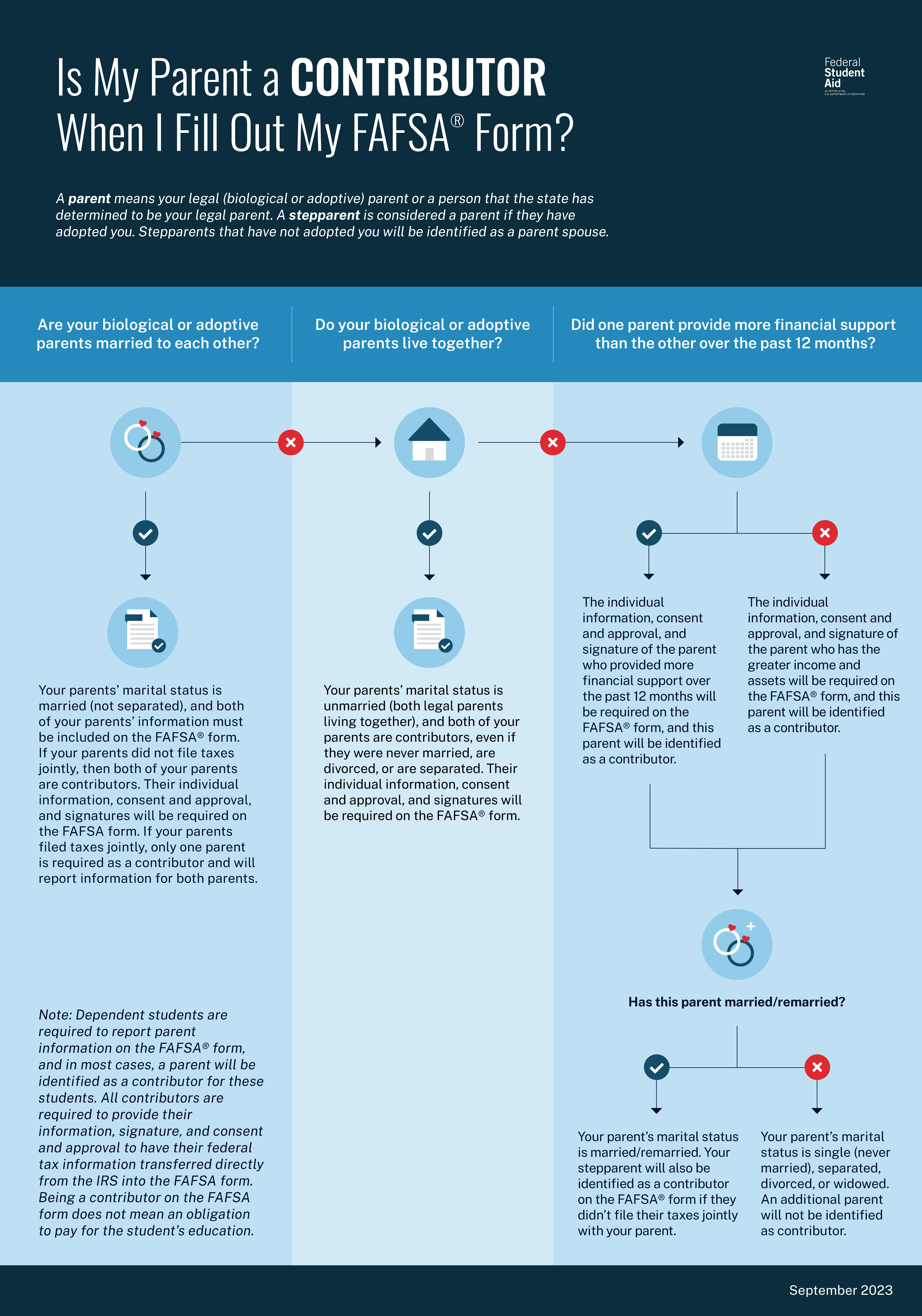

- FSA ID/Account: A login tied to your Social Security Number (or Alien Registration Number, if you’re a green card holder) that allows you to access StudentAid.gov, where you can complete the FAFSA and access federal aid and loan information. For dependent students, both the student and at least one parent or legal guardian (known as a “contributor”) will need to create an FSA ID; refer to this infographic for more information about who counts as a contributor.

- Note: Beginning with the 2024-25 FAFSA form, contributors who don’t have an SSN can now create a StudentAid.gov account.

- Financial Aid Direct Data Exchange: A tool used to import a family’s financial information directly from the IRS into their FAFSA form. Consenting to this process is now required to complete the FAFSA; see the US Department of Education’s guide to filling out the FAFSA for more information.

- Student Aid Index (SAI): A number representative of a family’s financial strength (based on a range of factors) that is produced by the FAFSA and used to determine financial need. The lower a student’s SAI, the higher their financial need (and the more federal aid they are likely to be eligible for).

- Note: This number is NOT a dollar amount of aid eligibility or what your family is expected to pay for college.

- FAFSA Verification: After submitting your FAFSA, your school may ask you to provide additional documentation to verify the information you provided on your form. This doesn’t mean you’ve done something wrong; once you provide the requested documentation, you should be good to go—but make sure to submit it by your school’s deadline!

- College Scholarship Service (CSS) Profile: A financial aid application administered by the College Board that is required by many (but NOT all) colleges; you can check if your school requires it by referring to this list on the College Board website. Students who complete this application may be awarded non-federal institutional aid.

Aid Offers

- Award or Offer Letter: A document from colleges, usually provided electronically in a student’s portal, that lists all federal, state, and institutional financial aid for which the student is eligible for that year. To see examples of what your aid offer letter might look like, check out the College Cost Transparency Initiative’s website.

- Note: Aid packages are awarded on a PER-YEAR basis, but funds are disbursed at the beginning of each semester.

How Do We Know Which Colleges We Can Afford?

It is essential that families have honest conversations about what they can afford before their student falls in love with a school. Doing your research in advance can help you avoid the heartbreak of finding a dream school only to later discover that your student’s first choice falls outside your budget; even worse would be making the financially irresponsible decision to enroll at that school. As a family, start having frank discussions about the following questions as early as possible and throughout the college admissions process:

- How much can we afford to pay out of pocket for college each year?

- How much can we afford to take out in loans? Will these be in the student’s name, parent’s name, or both?

- What is our bottom line? What cost will we rule out even if our student is accepted?

- What percentage of financial need is typically met by schools on our list?

- What will be the total cost of this college over four years? Will our debt be manageable?

- Based on our student’s field of interest, do we also need to consider graduate school costs further down the line?

- What are the pros and cons of our student working while in college? What would their earnings be used for? How many hours could they work each week?

To find out how much financial need a college typically covers, Google search “<college name> Common Data Set,” then scroll to Section H2 of the document. More financial aid information can be found throughout Section H. The US Department of Education’s College Scorecard is another great tool for browsing college statistics, including average net price based on various family income ranges. For an even more personalized estimate, families should complete the Net Price Calculator for each school on their student’s list. This tool can provide a general, simplified financial aid package example for that school, but keep in mind that your family’s package will likely differ from the package calculated by the tool.

What Kinds of Gift Aid Are Available?

- Scholarships: Scholarships are typically awarded based on a student’s merit, although some are awarded based on a student’s financial need. Check out our blog post on maximizing merit-based aid!

- Federal Pell Grant: Up to $7,395 per year awarded to families who have completed the FAFSA and whose calculated Student Aid Index (SAI) number is less than 7395 (i.e., the maximum Pell Grant award for the current award year).

- Federal Supplemental Educational Opportunity Grant (FSEOG): Limited funds ($100-$4000) awarded by some schools to students with exceptional financial need; award amounts depend on the availability of funds at a given school. Priority is given to Pell Grant recipients.

- State Grants: Visit NASFAA for more information about your state.

- Other Institutional Grants: Will have various names and appear on award letters.

What Kinds of Loan Aid Are Available?

- Federal Direct Loans: Low-interest federal loans in the student’s name that are awarded by completing the FAFSA. Repayment begins six months after college graduation, and flexible payment plans based on income are available.

- Subsidized: Awarded based on financial need; the government pays the interest on the loan while the student maintains at least half-time enrollment and up to six months after graduation.

- Unsubsidized: Available to all students; compounding interest accrues while the student is in school.

- For a more thorough comparison of subsidized vs. unsubsidized direct loans, see this article from the US Department of Education.

- Federal Direct PLUS Loans (also called Parent PLUS Loans): Federal loans that parents can apply for on their student’s behalf; repayment may begin immediately or, if you request a deferment, six months after the student graduates.

- Private: Provided by state agencies, banks, or other lenders; private loans have a wide range of interest rates and terms.

What Materials Do We Need to Apply for Financial Aid?

FAFSA:

- Parent and student FSA IDs

- Parent and student SSNs

- Tax returns

- Records of child support received

- Current balances of cash, savings, and checking accounts

- Net worth of investments, businesses, and farm

The FAFSA does NOT require information about:

- The home you live in

- Life insurance

- Retirement funds

- Cash already reported

- Non-owned Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) accounts

CSS Profile: (see if your schools require it)

- Tax returns (and all schedules)

- W-2 forms

- Records of any other current-year income

- Untaxed income and benefits records

- Assets information, including family-owned businesses

- Bank statements

- Information about the home you live in

- Value of retirement funds

When Do We Need to Apply for Aid?

The FAFSA and CSS Profile typically open on October 1 of a student’s senior year, but be aware that filing deadlines can vary widely: not only does each financial aid application have its own deadline, but each school will have its own financial aid deadlines and policies (and these may be different from a school’s deadlines for admission!). In the case of the FAFSA, the state the student is residing in may have its own financial aid application deadline as well.

The easiest way to find your deadlines is to Google search “<college name> FAFSA deadline” and click the link to the college’s website. In general, students should submit the FAFSA as early as possible but no later than March of their senior year in order to receive financial aid award letters in advance of May 1st, when they must choose where to enroll.

How Do We Compare Aid Packages at Different Schools?

After you submit financial aid applications and your student is accepted to a school, the college will send you a financial aid award letter that lists all federal, state, and institutional aid the student will receive. This financial aid award may be sent at the time of admission or some time after; timelines will vary by school.

Federal aid is the same for every school, while state and institutional aid can vary. For this reason, it is important to compare packages and not only determine if a school is affordable but also whether it is a fair deal. To see examples of what your aid offer letter might look like, check out the College Cost Transparency Initiative’s website.

Award letters typically have different formats and levels of detail, so it can be helpful to put all this information into a spreadsheet so it is easier to compare schools. You can use your school’s Net Price Calculator to quickly determine your net price for that school; if you’d prefer to calculate your net price manually, complete the following steps:

- Identify your Cost of Attendance (COA).

- Subtract any grants/scholarships from your COA.

- Finally, subtract out any loans to determine what your out-of-pocket cost will be, as well as your total indebtedness.

Remember: This is only for one out of four years, so it is essential to consider long-term costs and how they might change as your finances change.

It is always best to wait until you have all award letters in hand before making an enrollment decision. Even if you are happy with the package at your student’s dream school, you may be able to use offers from other colleges to negotiate more aid. Once you finalize your package, follow the necessary steps outlined in your award letter to accept the offer and enroll.

Common Misconceptions

Waiting until after January 1 to complete the FAFSA will result in more accurate aid because I can use my most recent year’s tax return.

To provide as accurate of a financial aid package as possible, the FAFSA uses “prior-prior” year taxes to calculate a family’s SAI. Families of students who will be going to college in Fall 2024 must use tax information from 2022 (not 2023) no matter when they apply. Major discrepancies between tax years can warrant an appeal once you receive your package; do not wait until January 1st to apply and risk missing a school’s deadline!

My SAI is 20000, so we can expect to pay $20,000 for college no matter where my student goes.

SAI is not what families are expected to pay for college. Rather, it is an estimate of what they could realistically afford. The gap between a family’s SAI and a school’s COA is their financial need, and colleges are not required to fill this gap with aid so that your bill matches your SAI. So, while you only have one SAI, you will have a different net price for every school.

Work-study shows up on my student’s award letter, so it will be credited to our account just like any other financial aid.

Colleges that list work-study in this way are tricky. Even if it looks like these funds are subtracted from your net price, they will NOT be automatically applied to your bill. These funds are awarded directly to the student in the form of paychecks for an on-campus job, so unless the student is saving all their checks for next year’s tuition bill, you should think of these funds as nothing more than pocket money.

- Note: Some schools WILL allow you to apply these funds directly to your school bill. Reach out to your school’s financial aid office to see if this is an option for you.

{kind=link}